Financial modelling

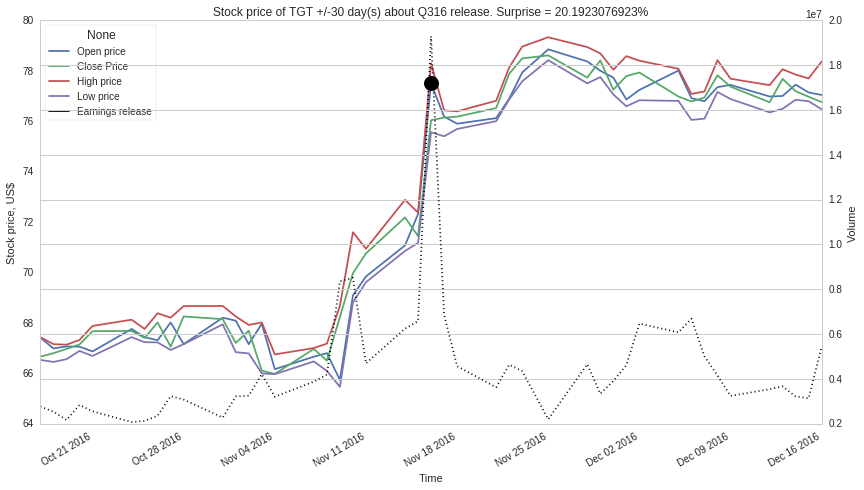

Stock price climbs in anticipation of good earnings. If earnings per share (EPS) beat Wall Street expectations, then depending on Surprise %, the price changes. The black dot represents the earnings report release. Image generated using Python.

In this project, my goal is to model and improve my investment strategy. I test the flaws, strengths and limits of the strategy.

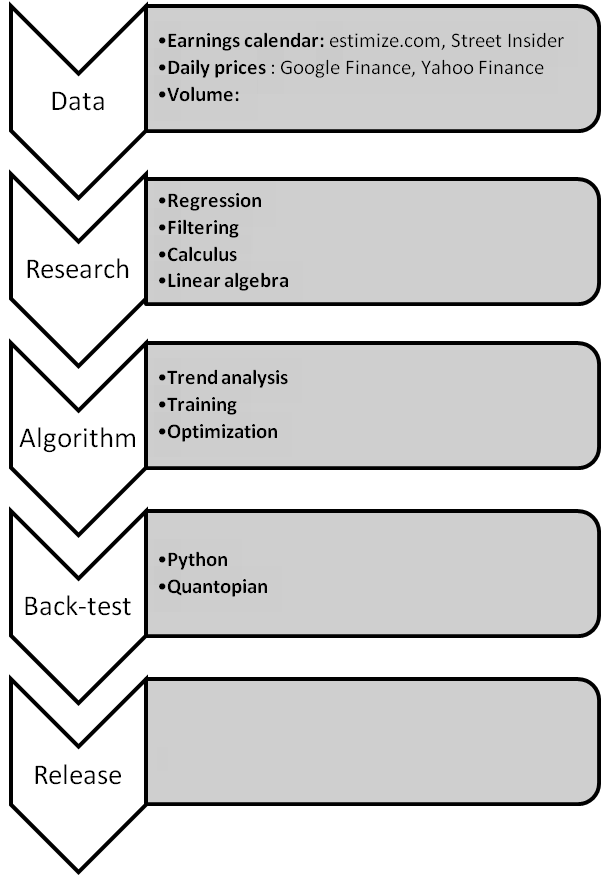

Flow chart of the steps I took in developing an earnings-based algorithm.

My research led me to Quantopian. It is an online platform that enables one to program trading strategies in Python and then back-test, live-test, live-trade and possibly license the same strategies. My draw to Quantopian was the availability of free-of-cost minute-by-minute stock price data and other data.

Through experience, I learned that programming the trading strategy outside the Quantopian platform can be very time-consuming. With your own code, you can be bogged down in tedious tasks such as fixing dates (line #56), plotting results (line #66), etc instead of focusing on the actual trading algorithm. I share a portion of my home-brewed program to show how tedious it can be. One can use zipline package to ease the pain.

Data acquisition

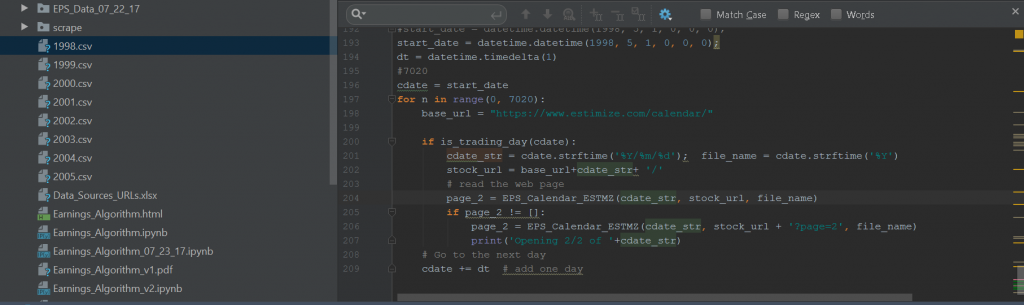

Using Python and iMacros scripts, I downloaded earnings calendars of 2,143 US companies starting from 1998 to 2020.

Screenshot showing one of many Python data-mining scripts I used to download earnings calendars. YES, I read and parsed over 20,000 html pages !! Thanks to Beautiful Soup.

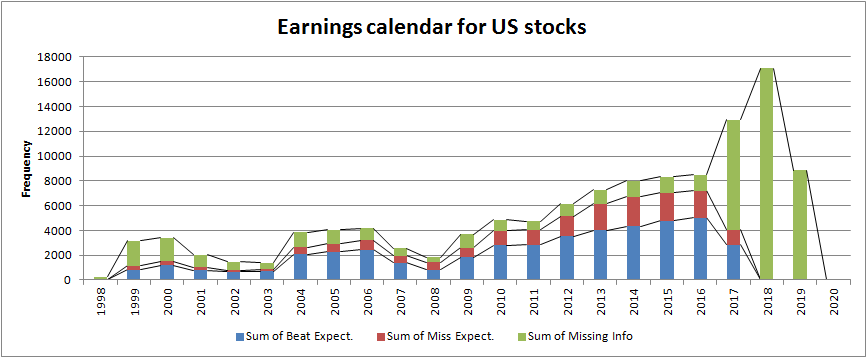

Summary of my earnings database. I still have missing information on 54,076 earnings releases (e.g. Wall St. expectations and actual EPS); a fraction of those have future release dates, i.e., Q3 and Q4 of 2017, 2018, and 2019. Of the 64,588 earnings releases with complete info, 70% beat market expectations.

Trend analysis

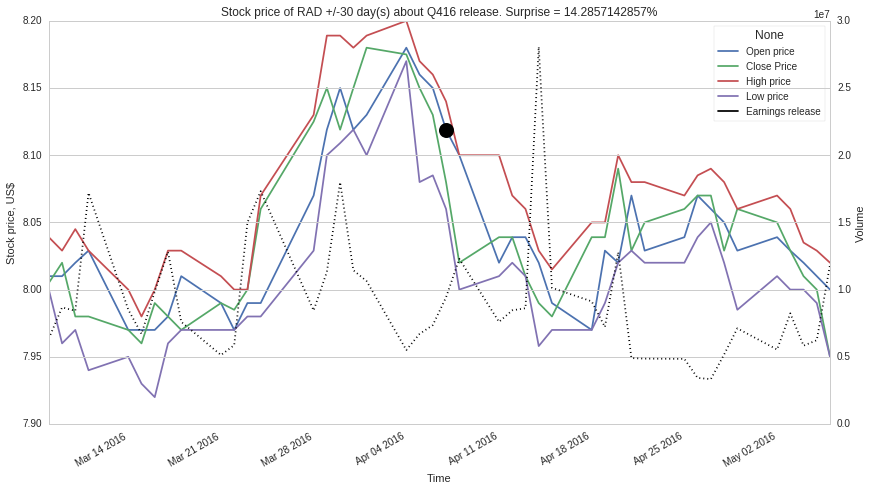

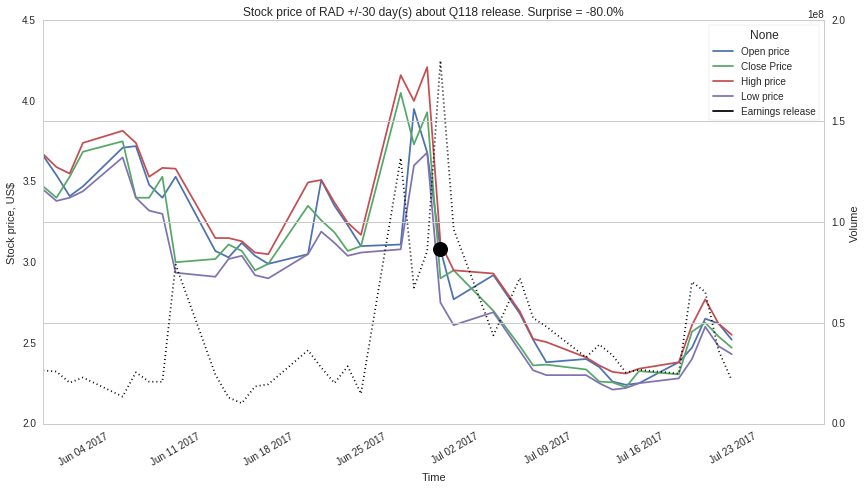

For a select companies, I analyzed historical stock prices around the earnings calendar. I find a few observable trends before and after earnings releases as I demonstrate in the figures below:

Stock price climbs in anticipation of good earnings. If earnings per share (EPS) beat Wall Street expectations, then, depending on Surprise %, the price changes.

Stock price climbs in anticipation of good earnings. If earnings per share (EPS) beat Wall Street expectations, then, depending on Surprise %, the price changes.

Regression

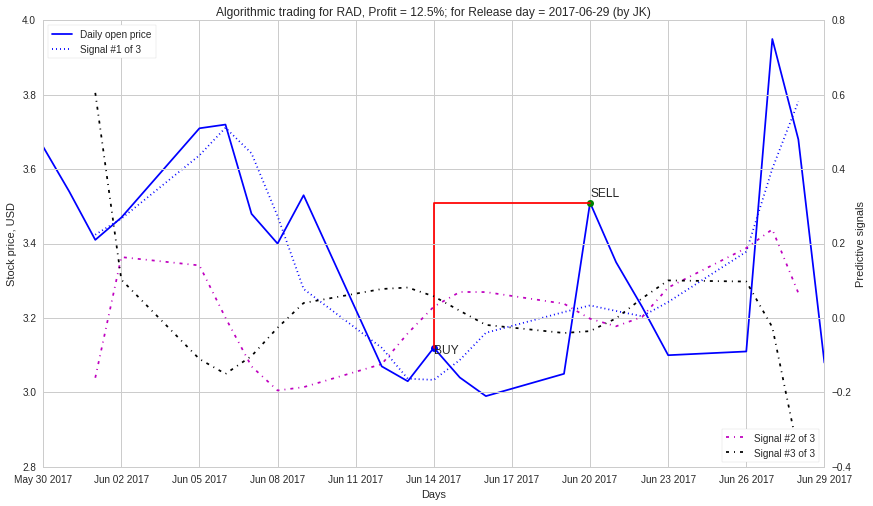

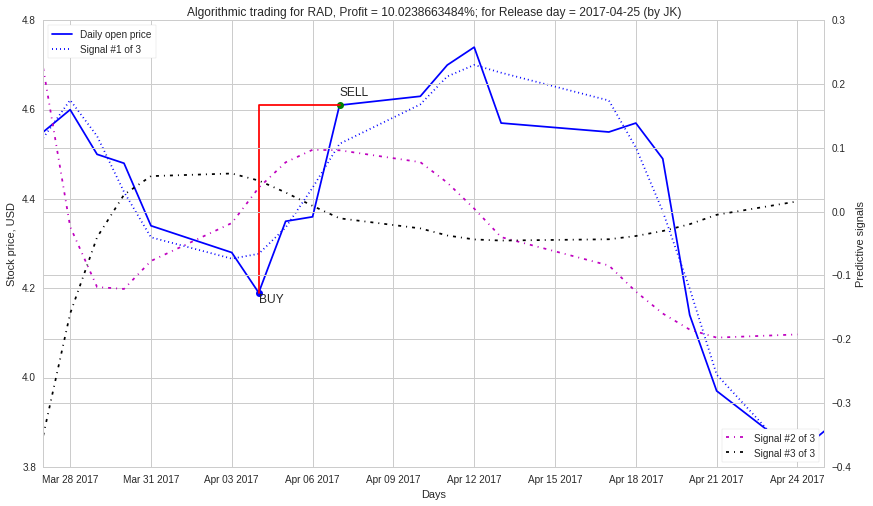

Here, I mathematically derived 3 signals to identify optimum buy and sell times before earnings release day. Some traders widely use the Moving Average Convergence Divergence (MACD) signal.

Simulated trade using my earnings-based algorithm. The buy/sell trades are executed days before a the release of quarterly earnings report. I use the signals (dotted lines) to decide.

Sample trade using my earnings-based algorithm. The buy/sell trades are executed days before a the release of quarterly earnings report.

Back-testing

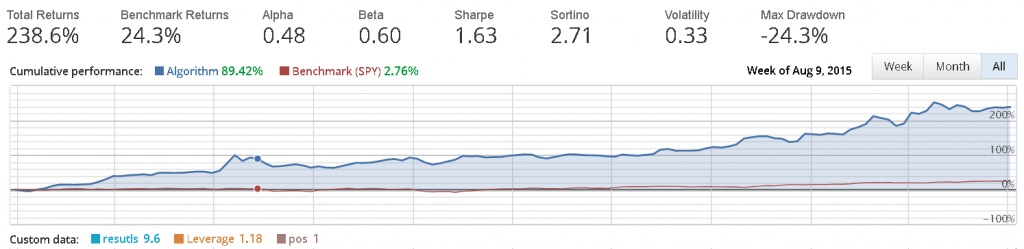

I am currently back-testing my earnings-based algorithm on Quantopian’s Python-based platform. A sample result is shown in the plot below. The platform executes the algorithm over a specified period, starting capital (US$ 10,000.00), type of securities, a set of stocks, commission and other brokerage fees and of course, the user-generated algorithm written in Python. Quantopian then outputs the total returns of the algorithmic trades among other variables.

Sample back-test results I did with a test algorithm from Jan-2015 to Jul-2017. Here, I used minute stock price data available on Quantopian. I use this platform to test trading strategies.

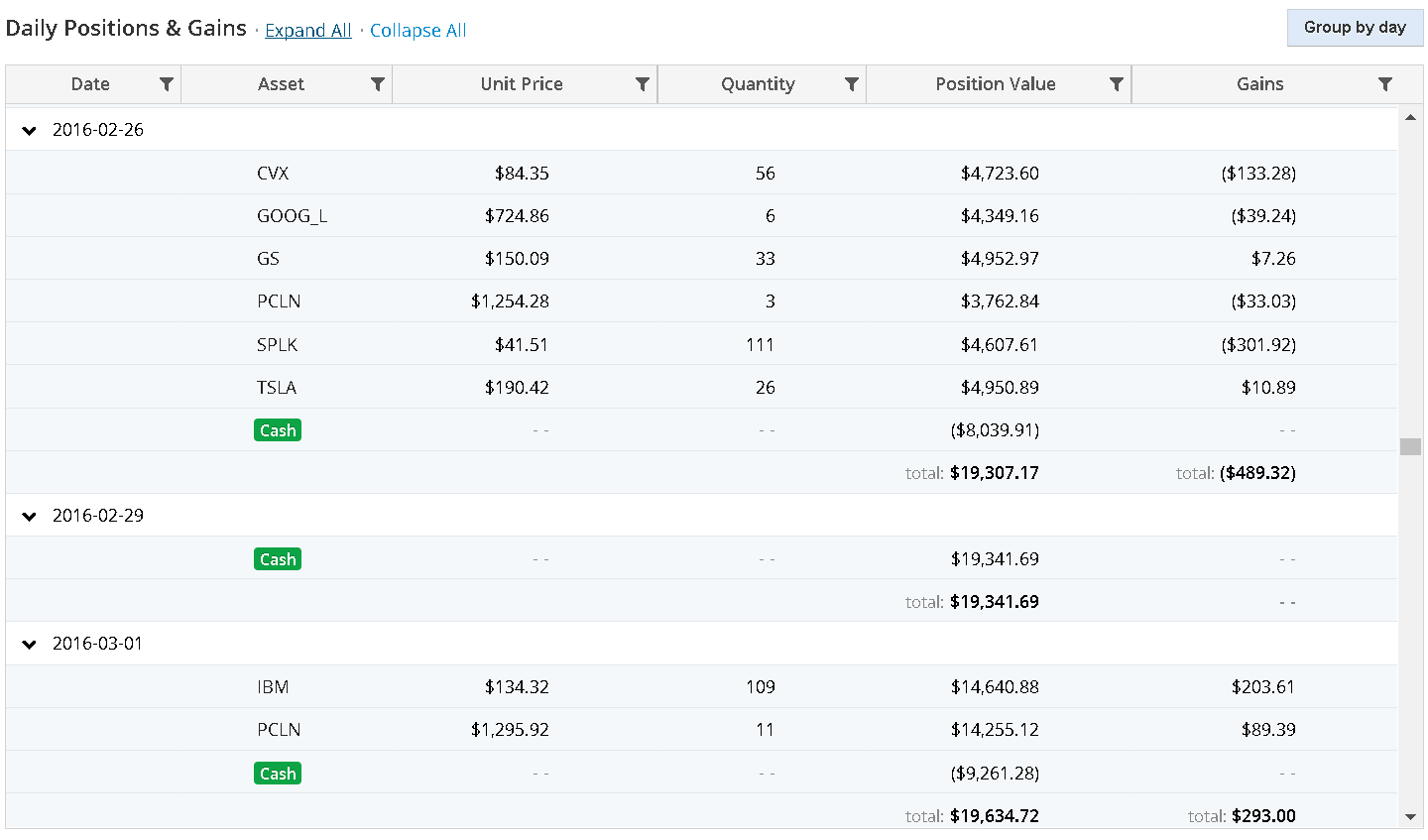

Sample back-test transactions with minute data. I did the simulation on Quantopian.

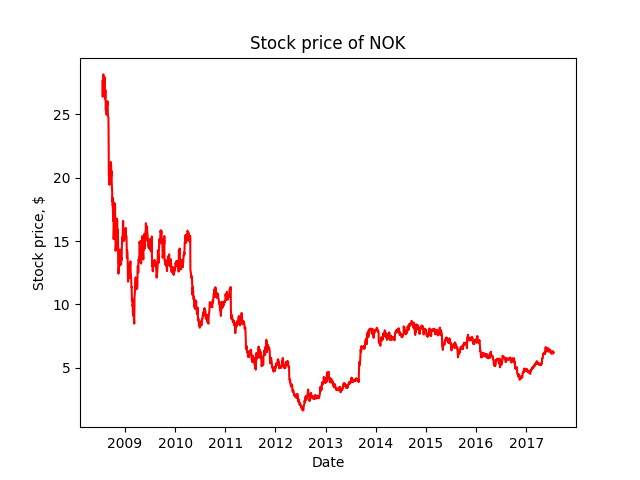

Example code of programming for finance in Python |

1 # Author: Jonah Kadoko 2 # Date: 07-19-17 3 # Description: 4 # The goal of this project is to be able to test specific trading algorithms using Python 5 6 import matplotlib.pyplot as plt 7 import matplotlib.dates as mdates 8 import datetime 9 import numpy as np 10 import urllib 11 12 def month2num(month): 13 # this function changes the month from letters to numbers 14 month_list ={ 15 'Jan' : 1, 16 'Feb' : 2, 17 'Mar' : 3, 18 'Apr' : 4, 19 'May' : 5, 20 'Jun' : 6, 21 'Jul' : 7, 22 'Aug' : 8, 23 'Sep' : 9, 24 'Oct' : 10, 25 'Nov' : 11, 26 'Dec' : 12 27 } 28 return month_list[month] 29 30 def stock_data(ticker): 31 fig = plt.figure() 32 ax1 = plt.subplot2grid((1,1), (0,0)) 33 # ticker = 'GOOG' 34 stock_price_data = [] 35 open_p = []; vol = []; close_p = []; trade_date = [] 36 stock_price_url='https://www.google.com/finance/historical?output=csv&startdate=Jul+20+2008&enddate=Jul+19+2017&q='+\ 37 ticker 38 raw_data = urllib.request.urlopen(stock_price_url).read().decode() 39 split_raw_data = raw_data.split('\n') 40 print(split_raw_data[0]+'\n') 41 42 for line in split_raw_data: 43 split_line = line.split(',') 44 if '\ufeff' in line or len(split_line) != 6: 45 print('debug_1') 46 else: 47 # print('debug_2') 48 # print(split_line[1]) 49 # stock_price_data.append(line) 50 open_p.append(float(split_line[1])) 51 close_p.append(float(split_line[4])) 52 if '-' in split_line[5]: 53 vol.append(0) 54 else: 55 vol.append(float(split_line[5])) 56 # Fix date and timing 57 split_date=split_line[0].split('-') 58 week_day = int(split_date[0]); 59 mon = month2num(split_date[1]); 60 yr = 2000 + int(split_date[2]) 61 date_temp = datetime.datetime(year=yr, month=mon, day=week_day) 62 trade_date.append(mdates.date2num(date_temp)) 63 # print(date[0].isoformat()) 64 # print(split_line[0]) 65 # print(stock_price_data[0:1]) 66 ax1.plot_date(trade_date, open_p, 'red') 67 plt.xlabel('Date') 68 plt.ylabel('Stock price, $') 69 plt.title('Stock price of '+ticker) 70 plt.show() 71 72 73 stock_data("NOK") 74

Stock price of Nokia Corporation from July 20, 2008 to July 20, 2017. I generated the plot using the Python code shown above.